Question: What must a regulated business in New Jersey or New York do after a ransomware event?

Answer: Regulated NJ & NY businesses must document incidents and notify relevant regulators per state and sector rules; maintain complete timelines and evidence to support insurance claims. Begin internal containment and forensic preservation immediately, then follow statutory breach-notification windows and sector-specific reporting rules.

This guide walks through post-ransomware compliance reporting nj ny step by step: who to alert, how to assemble evidence for cyber insurers, sector-specific obligations for financial and healthcare firms, and practical templates you can adapt. It targets website owners, marketers, and developers supporting regulated businesses, ensuring you understand which logs, timelines, and artifacts matter when regulators or insurers ask. For a comprehensive approach, consider our ransomware preparedness and recovery guide for NJ and NY businesses.

Overview of post-incident obligations for regulated businesses

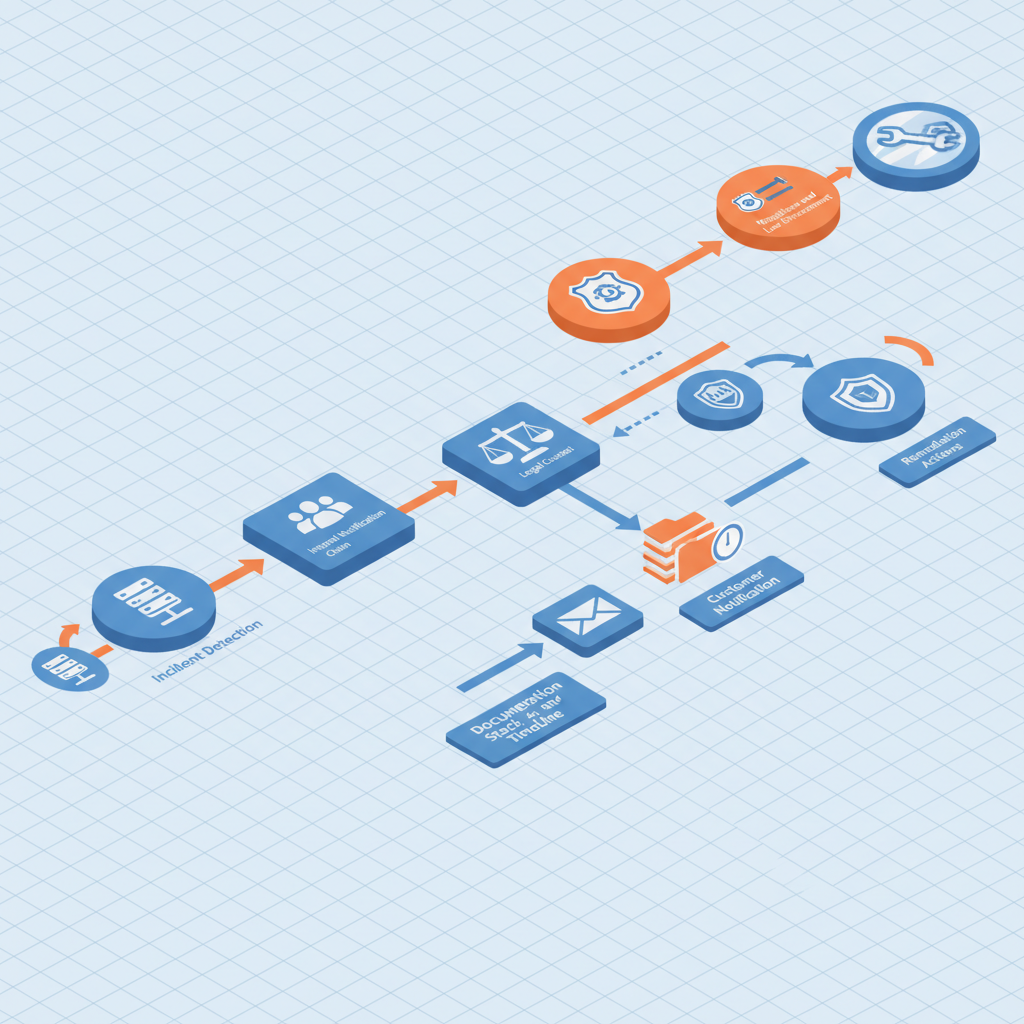

If a regulated company operating in New Jersey or New York suffers a ransomware incident, the first legal obligation is preservation: preserve logs, backups, and communications to avoid spoliation. The primary compliance tasks split into immediate technical containment, statutory notifications, and recordkeeping for insurers and auditors.

Start with these concrete actions within the first 24 hours: isolate affected systems; snapshot volatile evidence (memory, running processes); export SIEM logs for a minimum of 90 days; and take immutable backups of the encrypted data. For typical SaaS-style infrastructure, preserve endpoint detection and response (EDR) telemetry and server-side backups with integrity checks (hashes) and timestamps. For more on this, see Our pricing.

Regulated entities should map obligations against three categories: consumer data breach statutes (e.g., NJ breach-notification law), sector rules (for example, NYDFS for covered financial entities), and material incident disclosure rules (such as SEC guidance for public companies). Each has different triggers and timelines: some require notice when “unencrypted personal information” is accessed, others require reporting of incidents that materially affect operations or financial condition.

Practical example: a mid-sized marketing SaaS vendor with customers in NY detects a ransomware encryption event that affects customer data. The vendor should (1) document the attack timeline with timestamps and actor actions, (2) notify counsel, (3) determine whether regulated customer data was accessed or exfiltrated, and (4) prepare regulator and customer notifications per applicable statutes. Keep forensic images and a chain-of-custody log to show evidence was preserved.

Preserve evidence first: loss of logs or backups destroys insurer coverage arguments and weakens regulatory defenses.

Quotable definition: "Post-ransomware compliance reporting nj ny means collecting and reporting factual timelines, impacted data types, and mitigation steps to satisfy state statutes, sector regulators, and insurance claim requirements." Include a reference to New York's Department of Financial Services regulation when mapping requirements for covered entities (see References).

Who to notify and when — internal stakeholders, customers, regulators, and law enforcement

Notification responsibilities depend on the type of data exposed and the company's regulatory profile. Start by segmenting recipients: internal stakeholders (executive team, IT, HR, legal), customers and business partners, state regulators (New Jersey Division of Consumer Affairs for consumer breaches, New York Department of Financial Services for covered financial firms), and law enforcement (FBI/Cyber Task Force). Timing matters: notify internal stakeholders immediately; legal counsel should assess regulator triggers within 24–72 hours.

Use a notification decision table to determine scope. For consumer personal data exposures follow NJ's breach-notification statute if unencrypted personal data is accessed. For financial firms operating under NYDFS, report incidents that meet the regulator’s definition of a cybersecurity event — often within 72 hours of determining an event is reportable. If you’re a public company, follow SEC guidance for material incident disclosures.

Example notification timeline: Day 0 — containment and evidence preservation. Day 1 — internal executive and legal notification and initial assessment. Day 2–3 — determine whether notice to customers is required and prepare template notices. Day 3–7 — deliver regulator notifications if thresholds are met and file law enforcement reports if extortion or large-scale exfiltration occurred. Keep a recorded decision log noting the time each determination was made; regulators often ask when you knew what you knew.

Include these elements when you notify: a short factual summary (what happened, when), the categories of affected data, mitigation steps taken, and contact information for a designated incident liaison. For customers, explicitly state whether they should reset passwords or take specific remediation steps.

Internal notification chain and legal counsel involvement

Internal escalation must be fast and predictable. A recommended chain: IT/incident response lead → CISO/IT director → general counsel → CEO → board chair (if material). Legal counsel should join initial calls to guide privilege claims and regulator strategy. Privilege is central: route forensic reports through counsel to maximize attorney–client protection where appropriate.

Practical step-by-step: (1) Trigger an incident call within 60 minutes of discovery. (2) Create an incident action log with attendees and timestamps. (3) Assign a single public-facing incident liaison for all external communications. (4) Ask counsel to prepare privilege-aware forensic instructions to vendors to protect sensitive findings. Example: instruct forensic firm to deliver draft reports to legal counsel, not the broader IT team, to preserve privilege.

Communicating with customers and third parties (what to include)

Customer notices must be factual and actionable. Avoid speculation about root cause or attacker identity. The minimum content should include: (a) a concise description of the incident, (b) the data categories affected, (c) the estimated date range of the intrusion, (d) actions taken to contain and remediate, (e) recommended customer actions (password resets, monitoring), and (f) a contact point for inquiries.

Example customer notice template (short): "On [date], we detected a security incident that encrypted certain systems. We contained the incident on [date], and our forensic firm confirmed that email addresses and first/last names were accessed. We recommend you change passwords and monitor accounts." Attach an FAQ and provide a timeline of key events once available.

Third-party contract obligations can require rapid notification. Review vendor agreements for breach-notification clauses; some require notice within 48 hours of discovery. If your platform providers host critical backups, confirm integrity and availability before telling customers the extent of recovery options.

Working with cyber insurance: preparing evidence and timelines

Insurer claims hinge on documentation. Prepare a claim package that includes a forensic report, an incident timeline with timestamps, preserved logs and hashes, invoices for remediation, and a declaration of losses tied to the policy coverage sections (business interruption, ransom payment, forensic costs). Keep an organized digital binder with filenames and a one-page index.

Step-by-step evidence checklist for insurers: (1) preserve raw EDR and SIEM logs; (2) export firewall, VPN, and authentication logs covering the 30 days before and after the incident; (3) supply forensic images and chain-of-custody documentation; (4) document remediation actions and vendor invoices; (5) record internal communications about decision-making (who approved ransom payments or service engagements).

Concrete example: to prepare insurers for ransomware claim nj ny, export Windows Event Logs and EDR telemetry for affected hosts, provide immutable backup snapshots with SHA-256 checksums, and compile a timeline that records when each host showed symptoms and when it was isolated. Request the insurer’s preferred forensic vendors early; many policies require insurer approval for chosen vendors or impose notification windows that can void coverage if missed.

Insurers expect a complete timeline: missing timestamps or deleted logs jeopardize coverage more than the size of the ransom.

Quotable guidance: "Prepare insurers for ransomware claim NJ NY by delivering raw logs, signed chain-of-custody forms, and vendor invoices within the insurer’s required notice window." Consult your policy and insurer contact for exact submission timing.

Common insurer requirements and avoidable pitfalls

Common insurer requirements include timely notice (often within 72 hours of discovery), selection of approved forensic vendors, proof of reasonable cybersecurity controls pre-incident, and documented business interruption loss calculations. Avoid common pitfalls: delayed notification, altering logs, failing to maintain required MFA or endpoint protections, and inconsistent statements to insurers versus regulators.

Example pitfalls: a company that disabled EDR alerts after discovery and then restarted the system; insurers often see such actions as negligent and may deny coverage. Another pitfall is failure to produce prior security assessments — insurers commonly request pre-incident vulnerability scans, penetration test reports, or SOC 2 artifacts to evaluate coverage applicability.

Sector-specific reporting (financial services, healthcare, professional services)

Sector rules change what must be reported and to whom. Financial services firms in New York fall under NYDFS Cybersecurity Regulation (23 NYCRR 500), which requires covered entities to notify the superintendent of cybersecurity events that have a reasonable likelihood of materially affecting operations. The obligation may require submission within 72 hours after determining an event is reportable.

Healthcare entities must follow HIPAA breach notification rules for protected health information (PHI). If a ransomware incident involves PHI and meets the breach risk threshold, the entity must notify affected individuals, HHS OCR, and potentially the media for large-scale breaches. Keep forensic evidence that shows whether exfiltration occurred because risk of exposure drives notification obligations.

Professional services (legal, accounting) often handle client-confidential information. Client engagement agreements may require contractual notice and cooperation. Check professional ethical rules: lawyers may have additional duties to report breaches affecting client confidentiality and to document steps taken to protect client data.

Practical example: a New York financial-advisor firm detects ransomware and must evaluate whether customer account access or nonpublic personal information (NPPI) was exposed. If yes, NYDFS reporting and customer notifications may apply. For healthcare practices in NJ, determine if PHI was accessed and then follow HIPAA timelines and NJ state breach notification statutes for consumer data.

Documentation templates: incident reports, timelines, and remediation plans

Standardize artifacts so you can produce them quickly. Include these templates in your incident playbook: an executive incident summary, a technical incident report, a forensic evidence index, and a remediation plan with milestones and owners.

Incident timeline (required fields): timestamp (UTC), event description, host or user affected, action taken, owner, and evidence reference (file name/hash). Here’s a short incident timeline example row: "2025-03-17T03:12Z — suspicious PowerShell process spawned on WEB-01 — isolated host — evidence: web01_ps_0317.log (sha256:abc123) — owner: IT lead."

Use this post-incident regulatory checklist to produce consistent outputs:

- Preserve EDR and SIEM logs (export and hash).

- Create immutable backups and record SHA-256 checksums.

- Engage counsel and forensic vendor; document privilege routing.

- Produce a factual incident timeline with timestamps and owners.

- Assess regulator thresholds and prepare notifications.

- Compile insurer claim packet: invoices, timelines, forensic report.

- Publish customer notice and FAQ once facts are confirmed.

Also include a remediation plan template listing tasks, owners, deadlines, and verification steps. Example items: restore from verified backups (owner: IT, deadline: 72 hours), deploy updated EDR signatures (owner: MSSP, deadline: 24 hours), rotate privileged credentials with MFA (owner: security lead, deadline: 48 hours). Use measurable verification: "restore verified by checksum match and application smoke test (login test within 10 minutes)."

How MSP/MSSP partnerships speed compliance and insurer engagement

Partnerships with experienced MSPs or MSSPs accelerate evidence collection and communication. An MSSP that already collects centralized logs, maintains immutable backups, and retains forensic images reduces the time to respond. For New Jersey and New York entities, an MSSP familiar with NYDFS or HIPAA expectations can provide ready-made artifacts insurers and regulators expect.

Practical example: if you contract to a managed security provider that runs 24/7 SIEM and has a playbook for ransomware, they can export correlated alerts, provide attacker kill-chain timelines, and produce signed forensic exports with chain-of-custody. This capability shortens insurer review times and helps regulators see you had reasonable controls in place before the incident.

Step-by-step MSSP engagement checklist: (1) confirm MSSP provides EDR and SIEM data retention for at least 90 days, (2) ensure MSSP can produce immutable backup snapshots with verification hashes, (3) document escalation paths and approved forensic vendors, (4) agree on evidence-handling protocols that preserve privilege when routed through legal counsel. If you use external MSSP services, include contract clauses that require rapid evidence production and specify notification assistance during claims.

Post-incident remediation tracking and regulator audits

Regulators commonly request post-incident remediation plans and evidence during audits. Track remediation with a verified audit trail: store completion evidence (screenshots, logs, test results), attach vendor invoices, and document validation steps. For NYDFS or HIPAA, be prepared to show both technical fixes and governance changes (updated policies, training completion records).

Example remediation tracker table:

| Task | Owner | Deadline | Verification artifact |

|---|---|---|---|

| Restore encrypted servers from verified backups | IT lead | 72 hours | Backup snapshot hash & application smoke-test logs |

| Rotate all admin credentials and enforce MFA | Security engineer | 48 hours | Change logs and MFA enforcement report |

Keep a remediation evidence folder per task and reference it in your regulator response packet. Regulators will assess whether the post-incident controls reduce the likelihood of recurrence and whether the organization implemented recommended changes from the forensic report.

Recommended internal policies to simplify future reporting

Adopt clear policies that reduce friction during incidents. At minimum, maintain: (1) an incident response policy that defines roles and timelines; (2) a data classification policy identifying what constitutes regulated data; (3) a retention and logging policy that ensures SIEM and EDR data persist for at least 90 days; and (4) a vendor management policy requiring rapid evidence access clauses and defined notification windows.

Concrete policy thresholds: retain authentication logs and EDR telemetry for a minimum of 90 days; require backups to be immutable for at least 30 days post-incident; mandate quarterly table-top incident drills and annual full-scale recovery tests. Include a pre-approved vendor list for forensics and legal counsel to avoid delays during real incidents.

Example: add a clause to your vendor agreements that the vendor will supply requested logs within 24 hours of an incident declaration and will not delete or alter logs. This clause prevents disputes and helps you comply with "ransomware reporting requirements nj ny" by ensuring evidence is available when regulators request it.

Who this is NOT for

- Not for organizations without regulated data exposures (the checklist focuses on regulated-sector obligations).

- Not for entities that lack any logging or backup infrastructure — foundational work is required before these reporting steps apply.

- Not for groups seeking legal advice — the guide describes operational steps; consult counsel for binding legal interpretation.

Recommended next steps: codify these templates into your incident response playbook, test notification scripts during table-top exercises, and confirm evidence-handling workflows with your legal counsel and insurer contact.

FAQ

What is post-ransomware compliance, reporting & insurer readiness for regulated nj & ny companies?

Post-ransomware compliance, reporting & insurer readiness for regulated NJ & NY companies is the set of actions—evidence preservation, incident timelines, regulator and customer notifications, and insurer claim preparation—required to meet state statutes and sector rules while supporting insurance claims.

How does post-ransomware compliance, reporting & insurer readiness for regulated nj & ny companies work?

The process works by immediately preserving forensic evidence, escalating to counsel, assessing statutory thresholds, notifying regulators and affected parties when required, and compiling a complete insurer claim packet including logs, hashes, invoices, and a documented remediation plan.

References

- New York Department of Financial Services: 23 NYCRR 500 (NYDFS Cybersecurity Regulation)

- NYDFS Cybersecurity Resource Center

- CISA: Stop Ransomware Guide

- FBI: Ransomware guidance

- SEC: disclosure of cybersecurity incidents guidance

For hands-on help implementing the operational controls described here, consider reviewing the managed IT and cybersecurity offerings on our services or scheduling a demonstration on our services. To discuss a compliance or incident exercise, contact us, visit our contact us page, or contact us.